Every business exists to turn resources into goods and services that people want. In this topic, you will learn why businesses exist, how they are classified into different groups, and what it takes for a person to start and grow their own business.

1. Business Activity #

1a. Needs, Wants, Scarcity and Opportunity Cost #

People and countries have limited resources (such as money, workers, materials and land), but people’s needs and wants are unlimited. This problem is called scarcity.

Because resources are scarce, people and businesses must choose how to use them. Choosing one thing means giving up another. This is called opportunity cost.

A farmer has one field. She can use it to grow wheat or grow potatoes, but not both. If she chooses to grow wheat, the opportunity cost is the potatoes she could have grown instead.

1b. Specialisation #

Specialisation is important because it can make production more efficient. However, it also has some drawbacks.

| Benefits of specialisation | Drawbacks of specialisation |

|---|---|

| Workers become highly skilled at their one task, so quality can improve | Work can become repetitive and boring for workers |

| Production can be faster, since workers do not need to keep changing tasks | Workers can become too dependent on one skill, which is a problem if they lose their job |

| Less time is wasted moving between different jobs | If one specialised worker is absent, production may stop completely |

1c. Purpose of Business Activity #

Businesses take in resources, such as workers, materials, money and equipment, and use them to produce goods and services. This is the main purpose of business activity: to produce goods and services that satisfy the needs and wants of customers.

1d. Adding Value #

A business needs to add value so that it can cover its other costs and earn a profit. There are several ways a business can increase the value it adds to a product.

- Improving quality — better quality products can be sold at a higher price

- Branding — a well-known or trusted brand name lets a business charge more

- Design — an attractive or unique design makes a product stand out from competitors

- Convenience — making a product easier or faster to buy or use, such as through better locations or delivery

- Customer service — friendly, helpful service can make customers willing to pay more

A furniture maker buys wood costing $50 and uses it to make a chair. The chair is sold for $150. The value added is $150 − $50 = $100. If the maker improves the design and sells the same chair for $180 instead, more value has been added.

2. Classification of Businesses #

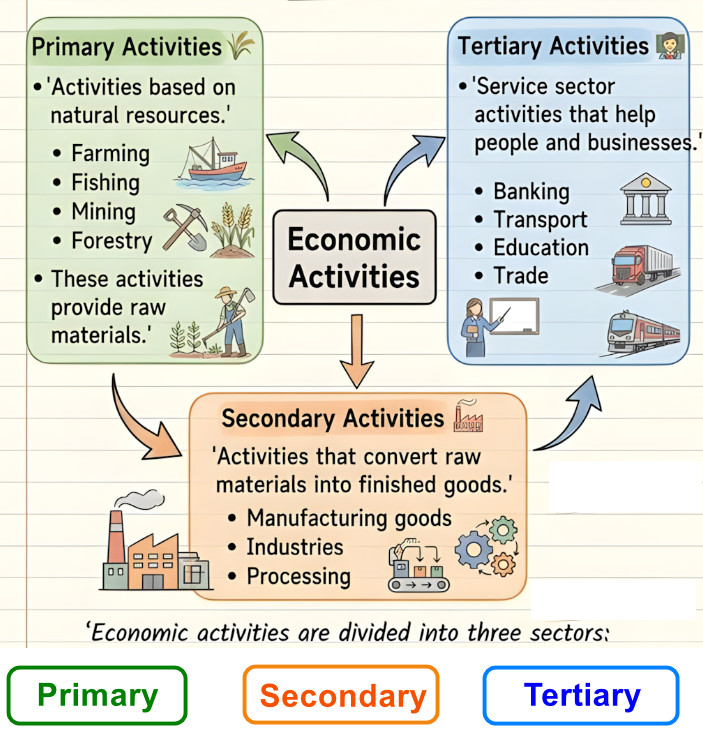

2a. Economic Sectors: Primary, Secondary and Tertiary #

Businesses can be grouped into three sectors, based on the type of activity they carry out.

| Sector | What it does | Examples |

|---|---|---|

| Primary | Collects or extracts raw materials directly from nature | Farming, fishing, mining, forestry |

| Secondary | Manufactures or builds things, turning raw materials into finished or part-finished goods | Car manufacturing, construction, food processing |

| Tertiary | Provides services to consumers and other businesses | Retail shops, banking, transport, education |

2b. Changing Importance of Business Sectors #

The importance of each sector changes over time as a country’s economy develops.

Reasons for this change include:

- New machinery and technology mean fewer workers are needed in the primary sector to produce the same amount

- As a country becomes wealthier, people have more money to spend on services, so the tertiary sector grows

- Developing economies often focus on producing and exporting raw materials, while developed economies focus more on services

2c. Private Sector and Public Sector #

In a mixed economy, businesses and organisations can be classified into two groups: the private sector and the public sector.

| Private sector | Public sector |

|---|---|

| Owned and controlled by private individuals or groups of people | Owned and controlled by the government |

| Main aim is usually to make a profit | Main aim is usually to provide a service for the public, funded by taxes |

| Examples: shops, factories, restaurants | Examples: state schools, public hospitals, the police |

3. Enterprise, Business Growth and Size #

3a. Characteristics of Successful Entrepreneurs #

Successful entrepreneurs tend to share several common characteristics:

- Innovative — able to come up with new ideas or improve existing products

- Willing to take risks — prepared to risk their own money and time, even though the business might fail

- Hardworking and determined — willing to work long hours and keep going despite difficulties

- Good organisational skills — able to plan and manage resources such as money, staff and time

- Good decision-making skills — able to make quick, sensible decisions, often with limited information

- Confident — believes in their business idea and can persuade others, such as investors, to support it

3b. Business Plans #

A business plan usually contains:

- A description of the business idea and what it will sell

- The objectives (aims) of the business

- Details about the target market and competitors

- A marketing plan, showing how the business will attract customers

- Financial forecasts, such as expected costs, sales and profit

- Details of how the product or service will be made or provided

- How much finance is needed and where it will come from

Business plans assist entrepreneurs in several ways:

- They help the entrepreneur to plan and organise the start-up carefully before spending any money

- They help identify possible problems in advance, so the entrepreneur can prepare for them

- They are often required to raise finance, since banks and investors usually want to see a business plan before lending money

- They set clear objectives and targets, which the entrepreneur can use later to check how well the business is doing

3c. Government Support for Business Start-ups #

Governments often support new businesses because start-ups bring benefits to the whole economy, such as creating jobs, increasing economic growth, and encouraging new ideas.

Governments support business start-ups in different ways, including:

- Grants — money given to a business to help it start up, which does not need to be paid back

- Training schemes — courses that teach entrepreneurs the skills they need to run a business successfully

A government wants to reduce unemployment in a town. It offers a grant to help a new entrepreneur open a factory, and provides a free training scheme to teach local workers the skills needed for the new jobs.

3d. Measuring Business Size #

Businesses come in many different sizes. There are several methods used to measure how big a business is.

| Method | What it measures |

|---|---|

| Number of people employed | How many workers the business employs |

| Value of output | The value of the goods or services the business produces, often measured over a period such as a year |

| Capital employed | The total amount of money invested in the business, used to buy equipment, buildings and other things needed to run it |

Each of these methods has limitations:

- Number of people employed — does not show that some businesses use a lot of machinery instead of workers. Such a business could produce a large amount with very few employees, making it look smaller than it really is.

- Value of output — it can be difficult to compare businesses that make different types of products, since prices and products vary so much.

- Capital employed — businesses in different industries need very different amounts of money invested, so comparing capital employed across industries can be misleading.

3e. Business Growth #

Many business owners want their business to grow larger over time. Reasons why owners may want to expand their business include:

- To increase profit and sales

- To reach more customers and gain a bigger share of the market

- To reduce the risk of the business failing, by offering more products or reaching more customers

- To gain a stronger position compared to competitors

Businesses can grow in different ways:

| Type of growth | How it happens |

|---|---|

| Internal growth | The business grows using its own resources and profits, for example by opening new branches or increasing production |

| External growth | The business grows by joining together with, or buying, another existing business |

Growth can also cause problems for a business:

- Communication problems — as a business gets bigger, it becomes harder for managers to communicate clearly with everyone who works there. This can be reduced by improving the way information is shared, for example through regular meetings or clear instructions.

- Loss of control — owners may find it harder to keep track of and control every part of a larger business. This can be reduced by giving trusted senior employees responsibility for different parts of the business.

- Cash flow problems — growth often needs a lot of money to be spent before the business earns extra money from the growth. This can be reduced by careful financial planning and arranging enough finance in advance.

Some businesses remain small on purpose. Reasons for this include:

- The owner wants to keep full control of the business

- The market for the product is small, so there is little demand for growth

- The business lacks the finance needed to grow

- The product or service depends on close, personal contact with customers, which suits a small-scale business

3f. Business Failure #

Not all businesses succeed. Both new and established businesses can fail.

Common causes of business failure include:

- Lack of management skills — owners or managers may not have the skills needed to run the business well, leading to poor decisions

- Changes in the business environment — things outside the business’s control can change, such as the economy, competition, or what customers want

New businesses are at a greater risk of failing than established businesses because:

- The owner usually has less experience running a business

- The business has not yet built up a base of loyal, regular customers

- It can be harder to get finance, since banks and investors see new businesses as more risky

- The business has no track record to show that its business plan will work in practice